General Sector-Specific Conditions

We supply products to a wide range of industries. Our main customers are in the semiconductor, photovoltaic, chemical, construction, electrical-engineering and electronics sectors.

Semiconductor Market Grows, But Silicon Wafers Decline

The semiconductor industry continued to grow in 2013. Demand for mobile end-user equipment, such as tablets and smartphones, compensated for the slow PC market. Market researchers at Gartner expect sales for 2013 to be up some 5 percent at US$ 315 billion. Weak PC business dampened demand for silicon wafers. Volumes slowed by –13.2 percent year on year to US$ 8.01 billion (2012: US$ 9.23 billion). Silicon-wafer demand, in terms of surface area sold, is estimated at about 58 billion cm 2. Overall, the market was flat for all diameters. Siltronic’s market share remained at about 15 percent.

Overcapacity, Price Pressure and Continued Growth Shape Photovoltaic Market

The photovoltaic market continued to expand in 2013. Various market studies and our own estimates anticipate that over 36.1 gigawatts (GW) of capacity were installed worldwide (2012: 31.1 GW), up 16 percent on the prior-year period. In Germany, feed-in tariffs depend on newly installed capacity and are reduced each month. As a result, the German market has declined, leveling out at 300 MW per month. According to Germany’s Federal Network Agency, the installed output reached 3.3 GW (2012: 7.6 GW). Other countries have supplanted Germany as the key market. China and Japan in particular recorded a marked increase in new installations.

Market conditions remained tight in 2013. Global production capacities still outstrip demand. Given the strong price pressure throughout supply chains, further companies became insolvent or exited the market. WACKER retained advance payments from long-term contracts and received damages from companies that withdrew from the business.

Additionally, markets were unsettled by anti-dumping proceedings by the European Union against Chinese solar companies and by the Chinese Ministry of Commerce against polysilicon manufacturers in the USA, South Korea and Europe. The European Union and China agreed in late July 2013 to set minimum prices for Chinese solar cells and to limit imports. The uncertainties in the anti-dumping dispute curbed production, especially at the beginning of the first quarter and in the third quarter of 2013. In the fourth quarter, we sold substantial volumes. Overall, WACKER sold greater quantities of polysilicon in 2013 than ever before, though at prices on a par with those at the end of the fourth quarter of 2012. Prices stabilized at this level in 2013. In total, we supplied 49,000 metric tons of polysilicon, including deliveries to our electronics-industry customers, a rise of 27.9 percent on the previous year.

Installation of New PV Capacity in 2012 and 2013

| Download XLS |

|

|

||||||||

|

|

Installation of |

Growth in 2013 |

||||||

|

|

|

|

|

|||||

|

|

|

|

|

|||||

|

|

2013 |

2012 |

% |

|||||

|

|

|

|

|

|||||

|

||||||||

|

Germany |

3,300 |

7,600 |

-57 |

|||||

|

Italy |

1,800 |

3,600 |

-50 |

|||||

|

Rest of Europe |

6,000 |

6,000 |

– |

|||||

|

USA |

4,200 |

3,300 |

27 |

|||||

|

Japan |

7,700 |

2,500 |

208 |

|||||

|

China |

11,000 |

4,900 |

124 |

|||||

|

Other regions |

5,000 |

4,000 |

25 |

|||||

|

Total |

39,000 |

31,900 |

22 |

|||||

|

|

|

|

|

|||||

Chemical Industry Without Economic Tailwinds – WACKER’s Chemical Divisions Record Stable Growth

In 2013, the chemical industry still did not show the momentum of previous years. Prices for chemical products decreased. Global output (including pharmaceuticals) in 2012 totaled € 4.1 trillion, with Asia contributing nearly 50 percent, Europe 25 percent, and the Americas 20 percent. The German Chemical Industry Association (VCI) expects chemical production in Germany to expand by 1.5 percent. Capacity utilization at German chemical plants was 84 percent. Sales edged up by 0.5 percent to € 187.7 billion (2012: € 186.8 billion). Growth was primarily driven by Asia. China remains the most interesting growth market. In 2012, chemical exports to China increased to € 5.4 billion. As a result, China now ranks among the top-ten export destinations for Germany’s chemical industry. Performance at WACKER’s chemical divisions remained strong, at the high level of 2012. Lower prices for standard products, unfavorable exchange rates compared with the previous year and the sluggish economy impeded growth. WACKER SILICONES recorded strong demand for silicone products for cosmetics, consumer goods, medical technology and industrial applications. WACKER POLYMERS again increased its sales of dispersible polymer powders. Business in dispersions, though, was weaker. At WACKER BIOSOLUTIONS, sales of polyvinyl acetate solid resin for manufacturing gumbase were at the prior-year level.

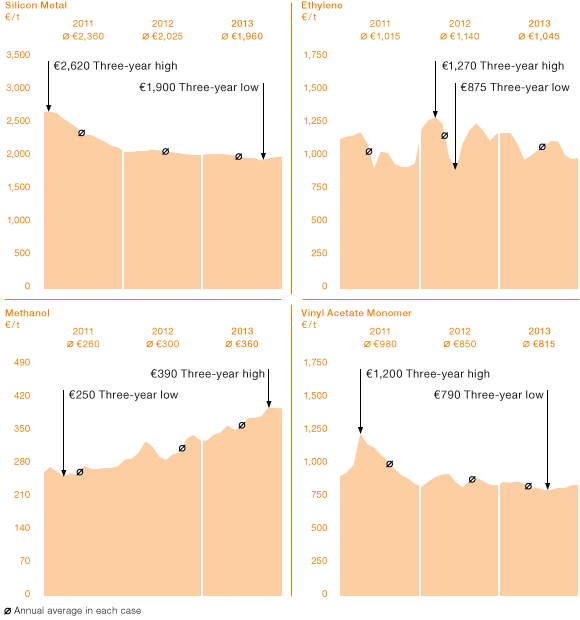

Spot-Price Trends for WACKER’s Key Raw Materials

Price trends for our key raw materials were not uniform in 2013. Silicon metal and VAM were only slightly cheaper, while ethylene prices in Europe fell by nearly 10 percent. The average price of methanol rose significantly by almost 20 percent throughout the year.

Construction Industry Grows in 2013

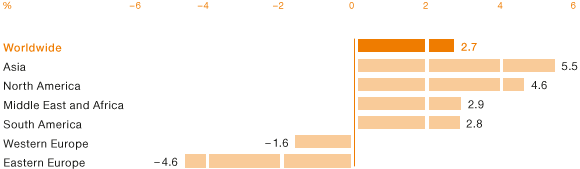

According to the market research institute Global Insight, the construction industry grew in 2013 by 2.7 percent globally to US$ 8.3 trillion (2012: US$ 8.1 trillion). In January 2013, the market researchers had still been expecting growth to come in at 4.1 percent. The effects of the euro crisis hurt the construction industry, especially in Europe, and led to a drop in construction contracts. Southern Asia again delivered the strongest performance, growing 5.5 percent. China – at US$ 1.8 trillion – remains the largest market worldwide. In the US, the property market continued to stabilize in 2013, spurring the construction industry, where volumes rose by 4.6 percent. In Western Europe, business declined by 1.6 percent. Sales in the German construction industry were US$ 323.8 billion in real terms (2012: US$ 323.8 billion).

Global Construction Industry by Region in 2013

Source: Global Insight

With construction applications, WACKER POLYMERS increased its sales further. Growth in dispersible polymer powders is driven by the market for dry-mix mortar in countries such as China and India. In these areas, we achieved double-digit sales growth. The move away from conventional building materials and construction methods to higher quality systems will continue. Europe’s prolonged winter dampened construction activity in the first half of 2013. In the second half, we did not fully make up for this decline, which meant that we posted a sales drop here. In dispersions, WACKER POLYMERS generated very strong growth in China, with dispersion sales for water-repellent flooring layers more than doubling. By substituting acrylates with VAE dispersions, we achieved over 40-percent growth in the sealant market in the USA. The European coatings market developed more slowly. Overall, we sold nearly 20,000 additional metric tons to the construction industry.

At WACKER SILICONES, construction-application sales were up by 3 percent. Raw materials for construction and silicones for building protection posted sales at the previous year’s level. Hybrid silicone products, on the other hand, saw business expand. In the case of hybrid polymers, which are used for example in wood-flooring adhesives, we increased sales by around 40 percent. Sales in cartridges under our own brand name also grew in certain countries, by around 7 percent. On the regional front, year-on-year sales were below the prior year in Germany (– 7 percent) and in Western and Southern Europe (– 2 percent). Sales in China grew by 4 percent. We grew in India (9 percent), the Middle East (23 percent) and the USA (10 percent). In Eastern Europe, business expanded by 9 percent.

Electrical and Electronics Industry Grows in Emerging Markets

With global sales of around € 3.6 trillion, the electrical and electronics industry continued its uptrend in 2013. The German Electrical and Electronic Manufacturers’ Association (ZVEI) estimates worldwide growth at 6 percent for 2013. The emerging markets were the main driving force here, expanding by around 9 percent. In Germany, the fifth largest market worldwide, sales edged up to around € 173 billion , according to ZVEI’s estimates (2012: € 170.2 billion). WACKER has three business divisions that supply customers in the electrical and electronics industries. At Siltronic, sales to semiconductor customers declined compared with the year-earlier period, mainly due to lower prices. During 2013, WACKER POLYSILICON sold around 15 percent of its polysilicon capacities to customers in the electronics industry.

WACKER SILICONES posted a sales increase of over 3 percent for this market. We generated higher sales in media-resistant potting compounds, in highly specialized silicone rubber grades for automotive electronics and optoelectronics, and in electronic components for circuit boards. The LED business remained at the prior-year level. In regional terms, sales rose in the USA (10 percent) and in Asia (8 percent). European sales came in at the year-earlier level.