Outlook for 2014

WACKER’s main assumptions in its planning relate to raw-material and energy costs, personnel expenses and exchange rates. For 2014, we are planning on an exchange rate of US$ 1.35 and ¥ 135 to € 1.

Performance Indicators and Value-Based Management

WACKER’s key financial performance indicators are unchanged compared with the previous year.

In 2014, WACKER will see its sales and EBITDA performance influenced by two decisions, both announced in January 2014. Siltronic’s acquisition of a majority joint-venture stake in Siltronic Samsung Wafer Pte. Ltd., in which Siltronic and Samsung had previously each held 50 percent, will positively impact sales and EBITDA trends. At WACKER POLYSILICON, the restructuring of the contractual and delivery relationship with one of its solar-silicon customers will have a positive impact of € 115 million on the division’s EBITDA and EBIT. Both these factors have been given due consideration in projections about WACKER’s development in 2014.

Group Sales and Volumes Set to Grow in 2014

WACKER expects volumes to rise at every division in 2014. In our planning assumptions, we anticipate that silicon-wafer prices will remain low (at levels below those of the prior year) and polysilicon prices will be somewhat above the prior-year level, with Group sales rising by a mid-single-digit percentage. For this forecast, we have also assumed that no trade barriers will be introduced for polysilicon shipped from Europe to China and that semiconductor demand will pick up in 2014.

Economic uncertainties mean the actual performance of the WACKER Group and its divisions could depart from our assumptions, either positively or negatively.

From today’s perspective, sales will climb at our chemical divisions and at WACKER POLYSILICON and Siltronic. We anticipate that Asia will deliver the biggest sales gains for our products. In 2015, sales should increase further compared with 2014 – provided that the world economy remains on its growth path, as predicted by business research institutes, and that there are no unforeseeable slumps in WACKER’s key regions and industries.

Outlook for 2014

| Download XLS |

|

|

||||

|

|

Reported in 2013 |

Outlook for 2014 |

||

|

|

|

|

||

|

Key Financial Performance Indicators |

|

|

||

|

EBITDA margin (%) |

15.2 |

Slight increase |

||

|

ROCE (%) |

2.2 |

Slight increase |

||

|

EBITDA (€ million) |

678.7 |

At least 10 percent higher |

||

|

Net cash flow (€ million) |

109.7 |

Balanced net cash flow |

||

|

|

|

|

||

|

Supplementary Financial Performance Indicators |

|

|

||

|

Sales (€ million) |

4,478.9 |

Mid-single-digit % increase |

||

|

Investments (€ million) |

503.7 |

Approx. 550 |

||

|

Net financial debt (€ million) |

792.2 |

Increase of between 300 and 400 |

||

|

|

|

|

||

|

Depreciation (€ million) |

564.4 |

Approx. 600 |

||

Outlook for the Key Performance Indicators at Group Level

From today’s perspective, the main key performance indicators at Group level will develop as follows:

EBITDA margin and EBITDA: the EBITDA margin should rise slightly compared with the previous year. Our projection is for EBITDA in 2014 to be at least 10 percent above its prior-year level as a result of higher volumes, further cost savings, first-time consolidation of Siltronic Samsung Wafer Pte. Ltd., and positive earnings effects due to restructuring of our contractual and delivery relationship with a solar-silicon customer. We anticipate continued price pressure for standard chemical products and silicon wafers. We expect a year-on-year improvement in Group net income amid higher depreciation and a tax rate of over 50 percent.

ROCE: our ROCE will edge up slightly compared with the 2013 figure of 2.2 percent.

Net cash flow: in 2014, we are aiming for a balanced net cash flow. Higher year-on-year investments and weaker positive effects from our inventory management will cause net cash flow to be substantially lower than last year.

Outlook for Supplementary Performance Indicators at Group Level

Investments: in 2014, investments are expected to total about € 550 million. The capital contributions made to acquire a majority stake in the joint venture with Samsung are not shown as investments, but as financing for the repayment of the joint venture’s financial liabilities. It is unlikely that the anticipated cash flow from operating activities will fully cover capital expenditures. Investments of a similar amount are budgeted for 2015. Depreciation will come in at about € 600 million in 2014. The majority-stake acquisition in the Samsung joint venture causes an increase of around € 80 million.

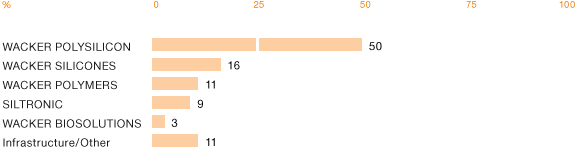

Investments by Division in 2014

Net financial debt: our net financial debt will increase year-on-year by about € 300–400 million (2013: € 792.2 million). This increase stems mainly from the acquisition by Siltronic of a majority stake in Siltronic Samsung Wafer Pte. Ltd. and from our polysilicon deliveries to customers for advance payments already received from them.

Divisional Sales and EBITDA Trends

At our chemical divisions, we posted what were, in some cases, one-time cost savings in 2013 that will not recur in this form in 2014.

At WACKER SILICONES, we anticipate substantially higher 2014 sales, with no significant pressure from raw-material costs, though the price squeeze on standard products will remain. The division’s volume growth in percentage terms is likely to outperform global GDP expansion. Growth will be generated mainly in Asia, where rising affluence is prompting higher per-capita consumption of silicone products. Additionally, ever increasing quality demands are accelerating the process of substituting simple products with value-added versions that incorporate silicones. We expect the steepest growth from products for personal care, for the electrical and electronics sectors, and for medical technology. EBITDA is projected to be slightly lower than last year, owing to the fact that the prior-year figure included a non-recurring effect in the amount of € 13.7 million (for reversal of a provision for purchase contract obligations in China).

At WACKER POLYMERS, we expect sales to climb substantially compared with last year. In dispersions, the main growth driver remains the shift away from styrene-butadiene toward VAE dispersions in the carpet sector in the USA and Western Europe. In emerging economies, we expect to see further growth in construction applications, especially interior paints. The regions with the highest sales growth are likely to be China, India and the Americas. We anticipate only a slight sales improvement in Europe. We will continue to pursue market strategies tailored to individual regions in order to fully harness growth potential. A slight year-on-year increase is expected in EBITDA.

At WACKER BIOSOLUTIONS, our projection is for substantial sales growth in 2014. We aim to step up our biologics business following the takeover of Scil Proteins Production. WACKER BIOSOLUTIONS now has a fermenter with a capacity of up to 1,500 liters. It can be used not only to manufacture pharmaceutical actives for clinical testing, but also for the market supply phase. We expect to see continued sales growth in the other segments (pharmaceuticals/agrochemicals and food) as well. We see the greatest growth opportunities not only in Asia, as before, but also in Germany. EBITDA is projected to come in at the prior-year level.

WACKER’s polysilicon business is expected to generate volume and sales growth in 2014. Our assumption is that the photovoltaic market will continue on its growth trajectory. Nevertheless, overcapacity is still a feature of the entire supply chain. We expect a very slight recovery in polysilicon prices for photovoltaic applications. However, our business could be adversely affected if the Chinese Ministry of Commerce were to impose punitive tariffs on European polysilicon manufacturers. Our main focus remains on achieving another substantial reduction in polysilicon production costs. Our EBITDA forecast is for substantial growth compared with the previous year. EBITDA performance will benefit from the restructuring of the contractual and delivery relationship with a customer from the solar sector. This will result in special income from retained advance payments and from damages received.

At Siltronic, we expect substantial sales growth in 2014, fueled primarily by the full consolidation of Siltronic Samsung Wafer Pte. Ltd., the joint venture that is now 78 percent owned by Siltronic. As previously, we anticipate that 2014 will see price pressure impeding sales growth. In the market for 300 mm silicon wafers, we expect continued growth. In the 200 mm and smaller-diameter segments, we forecast stable demand from today’s perspective. Our EBITDA projection is for a substantial increase on last year owing to consolidation of the joint venture.

Future Dividends

WACKER’s policy on dividends is generally oriented toward distributing at least 25 percent of net income to shareholders, assuming the business situation allows this and the corporate bodies responsible agree.

Financing

The main aspects of our financing policy remain valid. Even if the debt level rises further in 2014, we are confident that we have a strong financial profile with a sensible capital structure and healthy maturities for our debt. As of December 31, 2013, WACKER had some € 700 million in unused credit lines with maturities of more than one year.

Medium-Term Goals

At WACKER’s Capital Markets Day on July 1, 2013 in London, the company disclosed its medium-term targets through 2017 to the capital markets for the first time. Our focus for this period is on increasing the Group’s profitability and generating a positive cash flow.

WACKER’s Medium-Term Targets through 2017

| Download XLS |

|

|

||

|

|

Targets for 2017 |

|

|

|

|

|

|

Sales |

€ 6 billion to € 6.5 billion |

|

|

EBITDA |

€ 1.2 billion |

|

|

EBITDA margin |

Approx. 20 percent |

|

|

ROCE |

Over 11 percent |

|

|

Investments |

At the level of or below depreciation |

|

Executive Board Statement on Overall Business Expectations

Due to the positive projections, WACKER anticipates that the world economy will deliver stronger year-on-year growth in 2014. From today’s perspective, the global economy is expected to continue growing in 2015.

In 2014, we expect Group sales to rise, with all five business divisions increasing their sales. On the EBITDA front, our forecast is for substantial year-on-year growth of more than 10 percent, which will improve the EBITDA margin. The EBITDA trend will be influenced, though, by special income arising from the restructuring of our contractual and delivery relationship with a customer from the solar sector. This will result in special income from retained advance payments and from damages received. We anticipate that energy and raw-material costs – the main factors affecting cost of goods sold – will stay at the prior-year level. Price pressure is expected, particularly on silicon wafers and standard silicone and polymer products. In our polysilicon business, we assume that prices will rise slightly and that demand will pick up.

ROCE will edge up relative to last year.

Investments will be somewhat above the prior-year level at about € 550 million. Depreciation will be slightly higher at around € 600 million and thus higher than in the previous year. We are aiming to achieve a balanced cash flow. Net financial debt will climb by about € 300 – 400 million. Group net income should be higher than in the previous year.

WACKER supplies outstanding products and holds at least a No. 3 position in the markets of its four biggest divisions. The Group’s technological and innovative strength and its presence in key markets offer us a firm basis for reinforcing and even expanding our market positions.

After two years of steep price declines, particularly in polysilicon, we now see good prospects for growing sales and EBITDA in 2014. Given our current strategy, we also consider WACKER well equipped to continue growing profitably beyond 2014.

Up to the date of preparing the financial statements, nothing changed in our forecast.