Sector-Specific Conditions

We supply products to a wide range of industries. Our main customers are in the semiconductor, photovoltaic, chemical, construction, electrical-engineering and electronics sectors.

WACKER’s Chemical Divisions Report Good Sales Trend

In the chemical industry, the upward trend of the previous year continued, but lost some of its momentum. Prices for chemical products declined. Global consumption (including pharmaceuticals) totaled € 4.2 trillion in 2014, with Asia accounting for over 50 percent. The difficult international market environment also affected German chemical companies. According to the German Chemical Industry Association (VCI), chemical production in Germany is likely to have expanded by 1 percent in 2015. Low oil prices have helped make German producers more competitive, while the weak euro has bolstered exports. Capacity utilization at German chemical plants was 83.3 percent. With prices down 2.5 percent, sales were flat at € 190.8 billion (2014: € 190.8 billion). While the German chemical business achieved solid gains in the NAFTA region, demand in Europe declined even though industrial production there was stable. Exports to other regions did not compensate for this development, the main reason being slower growth in China and other emerging markets. WACKER’s chemical divisions posted higher sales year over year, mainly because of positive exchange-rate effects for all three divisions as well as volume growth and somewhat higher prices in a number of product segments. WACKER SILICONES recorded good demand for silicone products for electronics, consumer goods, the automotive sector and medical technology, as well as for industrial applications. WACKER POLYMERS substantially increased its sales of dispersible polymer powders and VAE dispersions. At WACKER BIOSOLUTIONS, revenue from sales of polyvinyl acetate solid resin for manufacturing gumbase rose as a result of price increases.

Construction Industry Grows in 2015

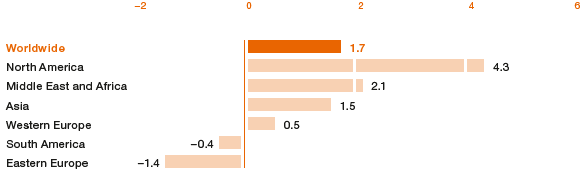

According to market research institute B+L Marktdaten GmbH, the global construction industry grew by 1.7 percent in 2015 to US$ 8.4 trillion (2014: US$ 8.3 trillion). Construction contracts in Europe stayed at a low level, rising in Western Europe by a marginal 0.5 percent. Sales in the German construction industry amounted to US$ 333.6 billion in real terms (2014: US$ 329.3 billion). Eastern Europe saw a decline in construction contracts of 1.4 percent. China – at US$ 1.8 trillion – remains the largest market worldwide. The North American real-estate market continued to stabilize in 2015, spurring the construction industry, where volumes rose by 4.3 percent. Asia, however, posted an increase of just 1.5 percent as the real-estate crisis in China took its toll.

Growth Rate of Construction by Region in 2015

Source: B+L Marktdaten GmbH

In construction applications, WACKER POLYMERS increased its sales further. Growth in dispersible polymer powders is driven by the market for dry-mix mortar in countries such as the USA and India and in regions like Southeast Asia and the Middle East. In these areas, we achieved double-digit sales growth. We also recorded further sales growth in Western Europe. Overall, we sold around 20,000 additional metric tons to the construction industry. As for dispersions, WACKER POLYMERS performed very strongly in Asia, especially in Southeast Asia and in China. Alongside adhesives and sealants, water-based, environmentally friendly coatings represent a key market for our VAE dispersions. At WACKER SILICONES, construction-application sales were up by 12 percent, with all three product segments – building protection, sealants and adhesives, and silane-modified polymers – posting gains. WACKER SILICONES grew 12 percent in sealants and adhesives, its largest segment. In 2015, sales rose in Germany and the rest of Europe, as well as in the USA and, particularly, in the Middle East. Sales were also higher in Asia, rising 12 percent. Our performance in India was particularly strong at over 38 percent. Sales in China grew by around 10 percent.

Electrical and Electronics Industries Grow in Emerging Markets

With global sales of approximately € 3.9 trillion, the electrical and electronics industries continued their upward trend in 2015 (2014: € 3.7 trillion). The German Electrical and Electronic Manufacturers’ Association (ZVEI) estimates worldwide growth at 5 percent for 2015. China and the other emerging markets are the main driving force here, expanding by around 7 percent. In Germany, the fifth-largest market worldwide, sales were up by about 3.4 percent and, according to ZVEI data, amounted to about € 178 billion (2014: € 172 billion).

WACKER has three business divisions that supply customers in the electrical and electronics industries. Siltronic’s year-over-year increase in sales to semiconductor customers was due to exchange-rate effects. WACKER POLYSILICON sold around 10 percent of its polysilicon volumes to customers in the electronics industry in 2015. WACKER SILICONES improved its sales in this market by 11 percent. The strongest growth was generated in Asia, where sales were 36 percent higher. We recorded sales growth in media-resistant potting compounds, in highly specialized silicone rubber grades and silanes for the semiconductor industry, and in silicone gels for automotive electronics. Sales in this segment were up 39 percent in China alone. The cable and insulator business also grew, with sales rising by 15 percent.

Photovoltaics Become a Mainstay of Global Energy Supply

The global photovoltaic (PV) market continued to grow strongly in 2015. According to various market studies and our own estimates, some 54 gigawatts (GW) of capacity were installed worldwide (2014: 44 GW). This is an increase of about 23 percent year over year, resulting in a total of around 230 GW in installed photovoltaic capacity worldwide at the end of 2015. Approximately 60 percent of new capacity was installed in China, Japan and the USA. The German PV market continues to shrink. According to the country’s Federal Network Agency, 1.5 GW of capacity was installed in Germany in 2015 (2014: 1.9 GW). But the industry is growing very strongly in many other regions, and photovoltaic systems are becoming a key mainstay of global energy supply – all of which is reflected in robust worldwide demand for PV modules. Key factors that have markedly spurred growth in PV installations are substantially lower costs for modules and continued incentives in several countries. Despite strong global growth in PV installations in 2015, market conditions in this industry remained difficult. Global production capacity throughout the supply chain still exceeded demand. Strong price pressure has prevented companies in this industry from achieving any substantial improvement in their financial situation.

Installation of New PV Capacity in 2014 and 2015

| Download XLS |

|

||||||||

|

Installation of New PV Capacity (MW) |

Growth in 2015 |

||||||

|

|

|

|

|||||

|

|

|

|

|||||

|

2015 |

2014 |

% |

|||||

|

|

|

|

|||||

|

||||||||

Germany |

1,500 |

1,900 |

-21 |

|||||

France |

1,000 |

900 |

11 |

|||||

Italy |

300 |

600 |

-50 |

|||||

Rest of Europe |

6,500 |

4,000 |

63 |

|||||

USA |

7,500 |

6,200 |

21 |

|||||

Japan |

10,000 |

9,300 |

8 |

|||||

China |

13,000 |

13,200 |

-2 |

|||||

India |

2,200 |

1,000 |

120 |

|||||

Other regions |

12,000 |

6,900 |

74 |

|||||

Total |

54,000 |

44,000 |

23 |

|||||

|

|

|

|

|||||

Planning certainty in the PV industry was negatively influenced by the anti-dumping proceedings and anti-dumping tariffs imposed by the European Union on Chinese solar companies and by the Chinese Ministry of Commerce on polysilicon manufacturers in the US, South Korea and Europe. In 2014, WACKER and the Chinese Ministry of Commerce (MOFCOM) had reached an agreement on the issue of polysilicon exports to China, in which WACKER undertook not to sell polysilicon produced at its European sites below a specific minimum price in China. MOFCOM, in turn, has refrained from imposing anti-dumping and anti-subsidy tariffs on this material. The agreement took effect on May 1, 2014, and is valid until the end of April 2016.

Growing Demand for Silicon Wafers

Demand for silicon wafers for the semiconductor industry grew in 2015 compared with the prior year. According to data of the trade association SEMI (Semiconductor Equipment and Materials International), global volumes – by surface area sold – rose by 3.3 percent year over year. Record volumes were recorded in each of the first two quarters. As the year progressed, however, volumes weakened as semiconductor manufacturers began adjusting their inventories. As a result, demand for silicon in the second half of the year was somewhat lower than in 2014.

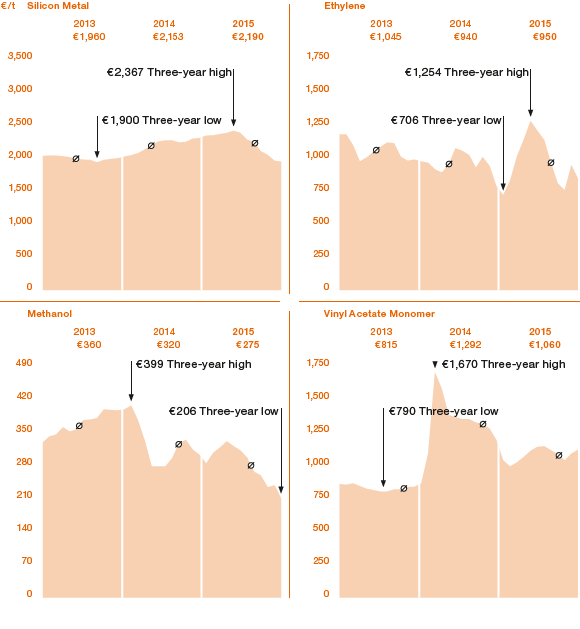

Spot-Price Trends for WACKER’s Key Raw Materials

Price trends for our key raw materials were not uniform in 2015. The price of silicon metal continued to rise in the first half of the year before declining steeply again toward the end of the year. On average, spot prices were up slightly year over year. The price of ethylene rose in Europe in the first half of 2015, before declining substantially in the second half. Over the year as a whole, prices remained at prior-year levels. In other regional markets, by comparison, spot prices were considerably lower year over year. Methanol was much cheaper compared with the prior year, with average annual spot prices being roughly 15 percent lower. After a strong rise in 2014, vinyl acetate monomer prices returned to more normal levels again, with spot prices down almost 20 percent. However, there was no return to the levels seen in 2013.